While the rest of the world has been witnessing plateauing growth for smartphones, India has been the only country to go against the trend and provides a glimmer of hope to OEMs across the world. However, painting a somber mood over the optimism surrounding the Indian mobile phone market has been a new report from CyberMedia Research. The overall shipment numbers for mobile phones in Q1 2016 has gone down, both on a YoY as well as on a QoQ basis. While the quarterly dip in mobile phone shipments numbers, from 60.5 million in Q4 2015 to 52.8 million of Q1 2016, can be explained as the yearly dip from the end of the festive season to the beginning of a new year, the 4.7% dip in growth YoY is what would trouble most readers.

But there is more to those numbers than what is apparent at the first glance. While on one hand smartphone penetration in India remains below 20%, cellular connectivity has reached more than 90% of the Indian population and as a result of that, slow down in the number of overall phone sales in the country is an expected aftermath. Things, however, look much brighter if we turn our attention to the smartphone side of things. With a 21.5% YoY growth, smartphone penetration looks to be increasing in India at a rapid rate. And despite India being heralded as a primarily budget market, the ASP (Average Selling Price) of smartphones in the country has increased steadily over the last year. How did this turnaround come to be? That is the question we seek to answer in today’s analysis.

Indian Smartphone Shipments Show Strong YoY Growth

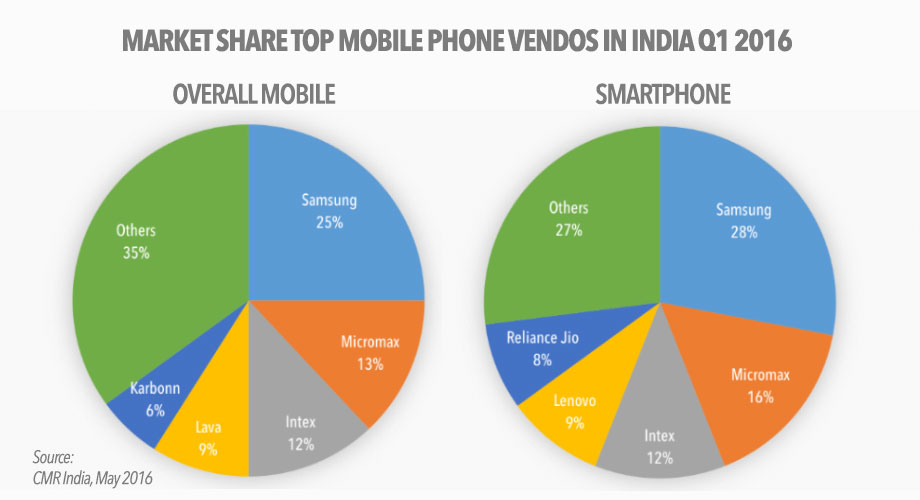

While feature phones make up the lion’s share of the market with nearly 55% of all phones shipped during Q1 2016, our focus today will be on their brethren, smartphone. Despite having 45% of the market share, they’re rapidly growing at a rate of 21.4% annum and will soon take over feature phones in the next few quarters. India, now the second largest smartphone market in the world, managed to ship 23.6 million smartphones in the first quarter of this year, undoubtedly an impressive feat, as the global market went through a slump. What was even more interesting though was the fact that 67% of the phones shipped during this period were from the Made in India initiative.

Despite strong pressure from the Chinese entrants, Indian brands managed to hold onto their own. In fact, Q1 2016 has been their best showing yet with 45% of the market share in their hands. With a YoY increase of 7% market share from Q1 2015, one must wonder if the Indian OEMs do stand a chance against the cheaper and better specifications offered by Chinese smartphones. For now, using offline distribution to their advantage, Micromax and Intex have managed to hold onto their 2nd and 3rd sport in the smartphone manufacturers chart. Samsung, of course, continues to assert their dominance by staying untouched at the pole position with 28% of overall market share.

While the regular players Micromax Intex and Samsung occupy the top 3 spots, Reliance Jio has been a new entrant that has burst onto the scene and quite literally taken it by storm. With every two out of three devices sold during this quarter belonging to the LTE category, it has been made quite clear that the Indian audience is showing a preference towards LTE handsets. While the sudden appearance of Jio Lyf, Reliance Communications LTE device arm has been explained in an earlier article, their presence in the top 5 along with that of Lenovo has reiterated the fact that to survive in the Indian market; OEMs must ship phones with 4G modems inside.

One of the characteristic traits of the Indian smartphone market has been their budget oriented mindset which has led to many OEMs participating in a rat race to the bottom for the cheapest smartphone possible. However, a few new entrants into the Indian smartphone market are looking to change all of that. And it looks like they may have struck gold as for the first time in history, the Rs 10-15k category was able to beat out the 6-8k price bracket in terms of sheer volume to take the No1 spot.

“We saw for the first time, price band of Rs 10,000 – 15,000 contributing the maximum (22%) towards the Smartphone shipments. Usually, the prime contributor used to be the price bracket of Rs 6,000 – 8,000.” said Faisal Kawoosa, Lead Analyst CMR’s Telecom Practice.

So why has the Indian smartphone consumer suddenly opted for pricier alternatives? For the answer, we had to travel as far East as China but for you, dear reader; the answer awaits in our finishing segment.

Final Thoughts

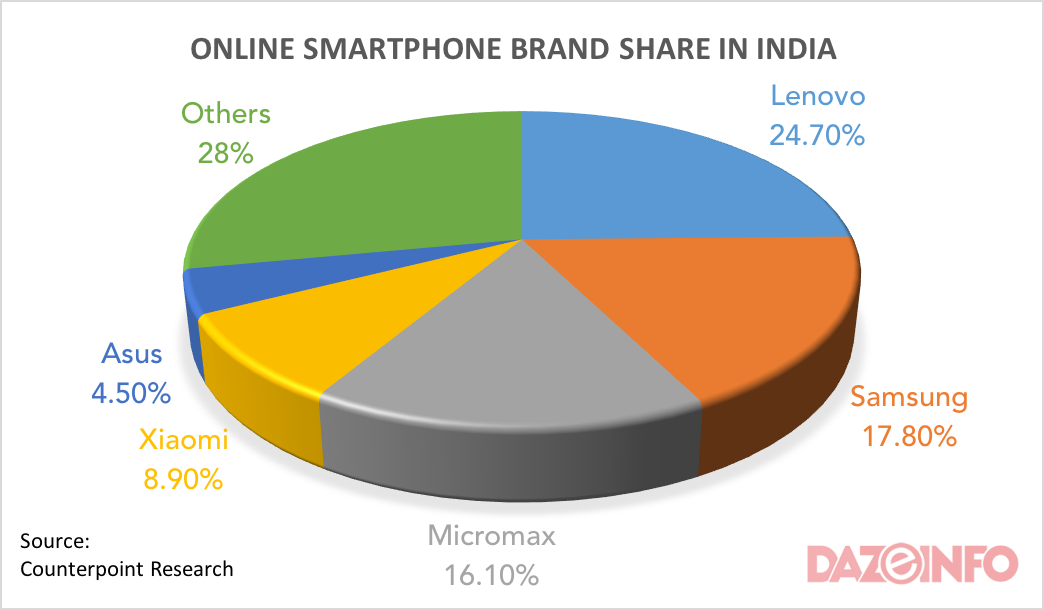

Before we begin elaborating on the comparison that we alluded to in our previous segment, let us first lay some groundwork for the current Indian smartphone scenario. Online sales have contributed for 1 out of every 3 devices that have been sold in the India market in the past year. Taking a look at the biggest players in this category and we find that the regular players like Lava and Karbonn have given way to newer players like Xiaomi, Asus, Lenovo among others.

These new players have found much success operating at a slightly higher price range of around 200$ where they can provide flagship competing specs at a very reasonable price point. Indian consumers who have always been very aware of ROI, has chosen to go for these slightly pricier but significantly more decked out devices. This is apparent as the smartphones that have done exceptionally well in this price band include Lenovo’s K4 Note, LeEco Le 1S, Micromax’s Canvas Mega 4G, Huawei’s Honor 5X and Intex’s Aqua Freedom.

With phones like Xiaomi’s Redmi Note 3 and LeEco’s Le 1s doing really well in the recent months, it seems that India’s online shoppers have upgraded their potential spending budget on phones. As most online shoppers are primarily based in Tier 1 cities, it can be expected that their spending power is higher than the country’s average. Added to that, smartphone proliferation in Tier 1 cities is quite high which means that many of the online shoppers are buying their second generation of smartphones. This slice of the Indian market bears a striking resemblance to the Chinese market, which in recent times has seen the meteoric rise of Oppo and Vivo, two OEMs who provide a unique smartphone experience albeit at a slightly more expensive price point.

The ASP or Average selling price of smartphones in Q1 2015 was a paltry Rs 10,364, a figure which has risen meteorically on a QoQ basis touching Rs 12,285 in Q4 2015 before finally settling in at Rs 12,983 in 1Q’16. And the driving force behind this has been the increased sales of handsets from companies like Lenovo, Oppo, LG, Panasonic, Micromax, Intex, LYF (RJio) and Vivo. The Indian smartphone scene at this moment has a very nice balance between domestic and foreign OEMs with 66% of the devices shipped in this quarter being assembled under the Made in India campaign. Even for LTE capable smartphones, 60% of them shipped during this period falls under the initiative.

However, despite the overwhelmingly positive quarter, few patches of ominous dark clouds remain. While mid-range devices have benefitted immensely from the Made in India campaign, yet the premium range of devices remains conspicuously absent from this initiative. But by far the fact that will cause the deepest furrow in a worried brow will be the fact that Micromax, India’s poster boy in the smartphone industry has been struggling in recent times.

“In the second quarter, we are waiting to see how Micromax performs after tweaking its brand logo and creating a new approach towards marketing and sales strategy,” says Krishna touching on this point of concern.

With the introduction of 4G LTE and global brands including Apple turning their eyes on India, a smartphone revolution is bound to happen! What remains to be seen is if the Indian OEMs can navigate the changing dynamics of their home market and escape unscathed.

{kind=link}