Mobile apps have become the cornerstone of our daily routines, reshaping the way we communicate, work, learn, entertain ourselves, and access information. Many companies, especially those in the realms of social media, gaming, and payment services, derive a significant portion of their revenue solely from their apps. To optimize monetization, mobile apps have embraced a hybrid approach, employing both advertising and in-app purchases (IAPs). According to the latest report from data.ai (previously known as App Annie), global mobile app spending exceeded $500 billion in 2022. Interestingly, of this mind-boggling amount, a remarkable 66.8% or $336 billion came from advertising, while the remaining 33.2% or $167 billion is derived from in-app purchases.

As the popularity and usage of mobile apps continue to soar, it is clear that advertising will remain a dominant force, further shaping the mobile industry and our digital experiences.

Here are some key insights into how advertising fuels the growth of the global mobile app industry, and the top players/companies that dominate the landscape:

Key findings: Mobile ad spend 2022

- Non-gaming apps have been driving advertising revenue within the mobile app landscape for years. Notably, they accounted for 65% of the total mobile ad spend market in 2022. This is roughly $220 billion out of $336 billion mobile ad spend. On the other hand, gaming apps accounted for the remaining 35% of the overall ad spending on mobile apps.

- Social media apps such as Facebook, Twitter, LinkedIn, Instagram, TikTok, YouTube, Snapchat, and Pinterest, have significant influence and market dominance in the advertising landscape. This can be understood by the fact that these owned-and-operated ad platforms alone accounted for 50% of the overall mobile ad spend in 2022.

- Among the social media apps operating on third-party ad networks like AdMob and AppLovin, communication apps emerged as the frontrunners in generating ad revenue.

- In the gaming app sector, hypercasual games accounted for most of the total mobile ad revenue in 2022. This is followed by other casual genres like Puzzle and Simulation, which played a significant role in ad revenue generation. These genres attract players who enjoy strategic thinking, problem-solving, and immersive experiences.

- In the United States, Zynga’s Words With Friends 2 has established itself as the market leader for word games, particularly in terms of average ad revenue per user. The game generated an average of $1.80 per monthly active user in Q1 2023 across AdMob, Vungle, AppLovin, UnityAds and ironSource ad networks.

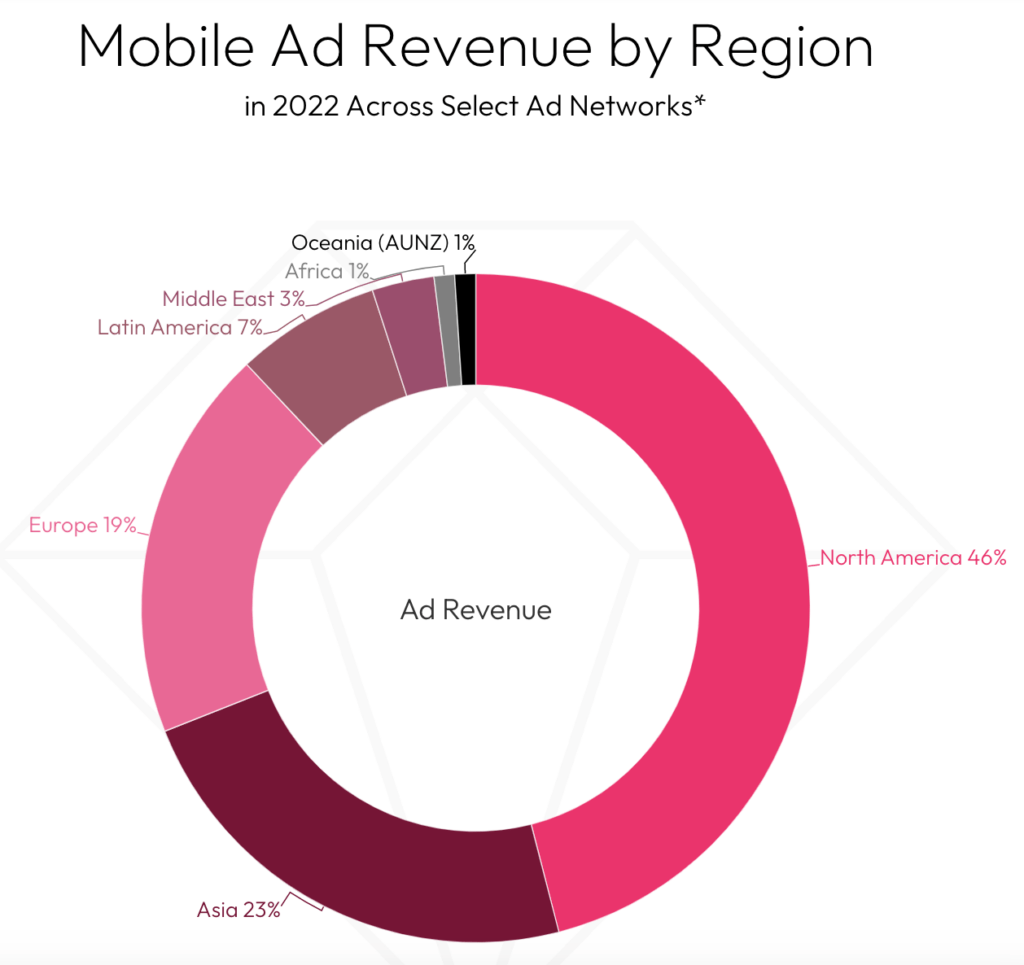

- North America accounted for nearly 46% of the global mobile ad revenue in 2022, across selected ad networks (AdColony, AdMob, AppLovin, ironSource, UnityAds, Vungle). Within North America, the United States stood out as the top country for ad revenue, holding a prominent position on both iOS and Android platforms.

- Despite Asia’s rapidly growing mobile market and a significant number of smartphone users, it is surprising that the region (excluding China) accounts for only 23% of the global ad spend on mobile devices. This indicates that there is still untapped potential for advertisers to explore the Asian market.

- Europe boasts a mature advertising market, with countries like the United Kingdom, Germany, and France exhibiting high smartphone penetration rates and digital connectivity. Despite this, Europe accounted for approximately 19% of the global mobile ad revenue in 2022.

*Ad revenue includes a subset of ad networks and excludes social media and OTT. Included networks are: AdColony, AdMob, AppLovin, ironSource, UnityAds, Vungle

In a nutshell

Advertisements offer a way to generate revenue from a broader user base, including those who may not make in-app purchases or prefer to engage with the game without spending money.

Advertisers and businesses continued to invest in mobile advertising, recognizing its effectiveness in reaching and engaging with a mobile-centric audience. Despite facing significant challenges such as the General Data Protection Regulation (GDPR) in Europe and Apple’s App Tracking Transparency, mobile ad spending not only represents a larger portion of total app revenue but also experienced an impressive 14% YoY growth in 2022.

It is no surprise that social media companies like Facebook, Snapchat, etc., heavily rely on advertising as their primary source of revenue. In 2022, Facebook, for example, generated 97.5% of its global revenue from advertising alone, amounting to $113.6 billion. Meanwhile, Snapchat also generated approximately $4.6 billion in revenue during the same period by offering various advertising products on Snapchat, which include Snap Ads and AR Ads.

In a significant move, Netflix, the global leader in over-the-top (OTT) streaming, also introduced a cheaper subscription plan called ‘Basic with ads’ in October 2022. This decision was driven by the fact that Netflix is facing strong competition in the streaming landscape and aims to differentiate itself in a crowded market. While Netflix has primarily relied on subscription fees as its revenue source, the inclusion of ads in this new plan demonstrates the company’s willingness to explore alternative monetization strategies.

The biggest challenge for these companies is the constant need to innovate their advertising offerings in order to meet the evolving needs of advertisers and deliver a valuable user experience.

Twitter, on the other hand, has been losing the game in the advertising business. Following its acquisition by Elon Musk, Twitter’s ad revenue has sharply declined. The decline in ad revenue, however, aligns with the strategic vision of the CEO, who aims to reduce dependence on ads and transition towards a more secure subscription-based model.

{kind=link}