The prevailing technological trend over the past decade has been the shift towards mobile solutions. Our devices are shrinking down, and everything is becoming much more portable. In such a world, it stands to reason that the internet is also becoming increasingly mobile. The internet forms the backbone of much that we use modern technology for. As the technology has become mobile, so has the internet in order to keep up.

A new report, titled “ICT Facts And Figures” by ITU outlines the ongoing global shift towards mobile broadband solutions and the general state of broadband connectivity across the world.

Let us dissect the facts in the report and analyse the state of broadband connectivity, both mobile and fixed, across the world.

The Internet Is Becoming Mobile

The biggest feature of the ITU report is the exploding popularity of mobile broadband. From 2012 to 2017, mobile broadband subscriptions have grown more than 20% annually, across the world. According to estimates, the total number of mobile broadband subscriptions to top 4.3 billion globally by the end of 2017! The highest growth has been coming from non-developed regions. In the past five years, mobile broadband subscriptions have grown at a tremendous rate of around 55% YoY in LDCs (Least Developed Countries). Growth in developing countries has been similarly high, with over 30% YoY growth rate.

As a result, mobile broadband penetration has gone up too. There will be 60 mobile broadband subscriptions for every 100 inhabitants globally by the end of 2017. Penetration is still relatively small in developing and LDC regions, however, the high growth rates will change that in the coming years. Penetration in developed regions is sky high, with over 95 subscriptions per 100 inhabitants. This saturation accounts for the rather low growth rate in these regions.

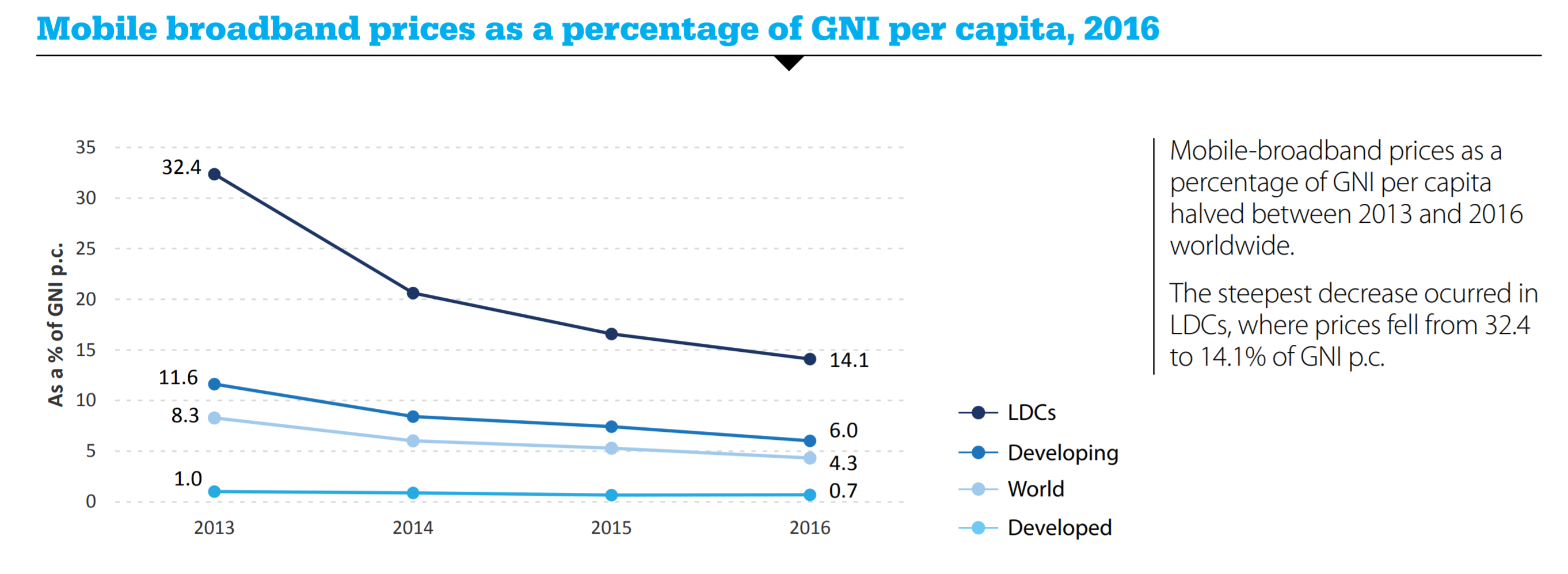

Mobile broadband is not only more ubiquitous, but it is also cheaper. The average prices for mobile broadband have fallen in all regions over the past five years. The sharpest fall in prices has occurred in LDC regions. Meanwhile, the already low prices in developed countries have remained mostly stagnant. The falling prices and increasing availability of faster mobile broadband networks have spurred an internet revolution off sorts in many developing regions. Take the case of the Asia Pacific region. According to reports, by 2020, 50% of global 4G subscribers will come from the largest developing APAC region.

The example of India typifies the tremendous growth in APAC. While the country has had access to mobile broadband for a few years now, adoption exploded over the past year with the launch of Reliance Jio. It’s cheap tariffs, and ubiquitous availability led to rapid growth, resulting in 100 million subscriptions in record time. Now, nearly 92.8% of all broadband subscriptions in the country come from mobile.

Fixed Broadband Is Suffering At The Hands Of Mobile

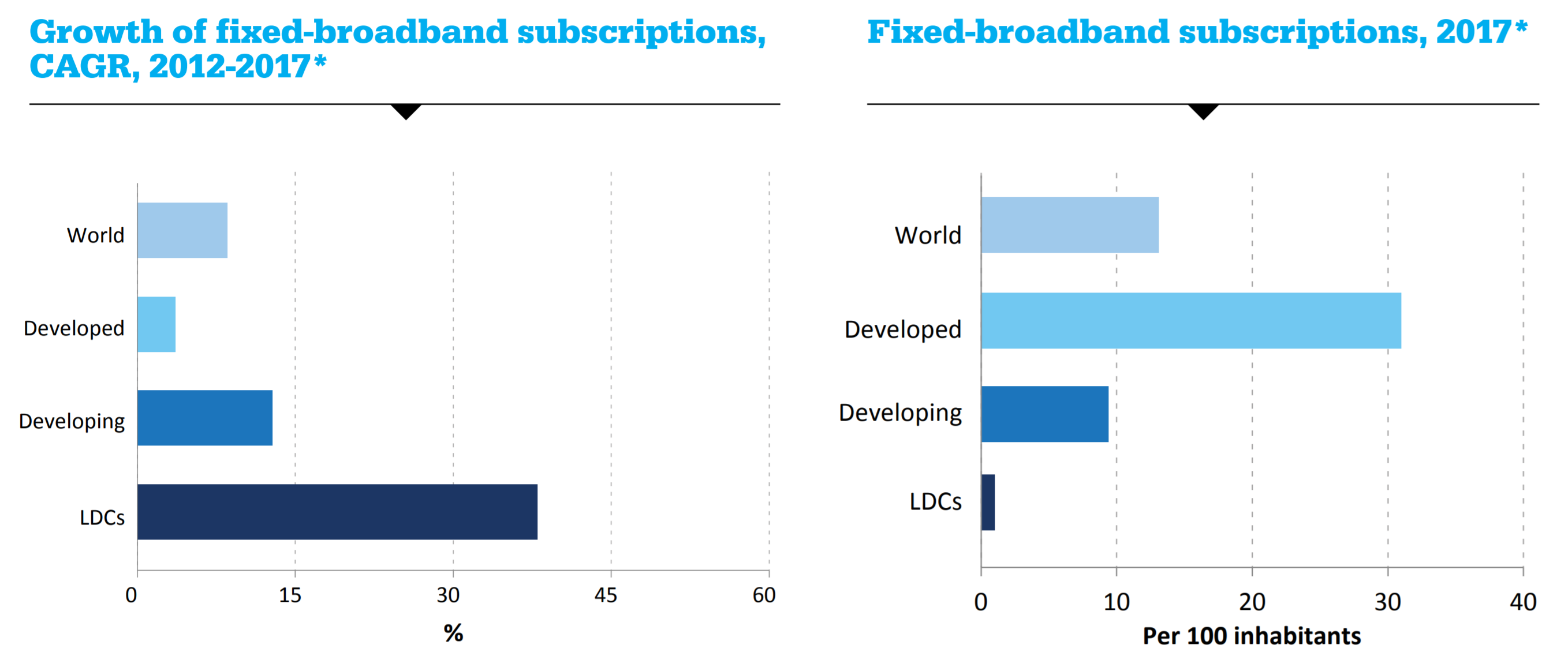

A cursory glance at the subscription statistics from 2012 to 2017 make one thing amply clear; Fixed broadband subscription growth leaves much to be desired. The annual growth rate for fixed broadband globally was a mere 9% during this period. However, this number is highly skewed by the non-developed world. The growth rate for developed countries was less than 5%, while the growth rate in developing countries was only a little over 10%. In fact, the majority of growth in fixed broadband came from LDC regions in the last five years. LDCs drove global fixed broadband adoption with an annual growth rate of just under 40%.

So what is the reason behind the lethargic growth rates for fixed broadband?

One reason could have to do with rising saturation in developed countries. By end of 2017, there will be over 30 fixed broadband subscriptions for every 100 inhabitants in developed countries. This number, coupled with the phenomenal growth and penetration of mobile broadband highlights a significant growth potential in the developed world.

In contrast, developing countries will have less than 10 fixed broadband subscriptions for every 100 inhabitants. The situation is even more extreme in LDCs, with only 1 fixed broadband connection for every 100 inhabitants by the end of 2017. This data demonstrates that there is tremendous potential for growth in these regions. Despite the potential, however, growth has been underwhelming. The primary factor behind this is Cost. Mobile broadband prices were less than 5% of GNI per capita in 73 developing countries, along with 3 LDCs. However, fixed broadband prices were less than 5% of GNI per capita in only 61 developing countries and 2 LDCs. Fixed broadband adoption in developing countries is adversely affected by the higher cost vis-a-vis mobile broadband.

In LDCs, both mobile and fixed broadband remain inordinately expensive, with pricing being more than 5% of GNI per capita in nearly all surveyed countries. However, the price gap between fixed and mobile is even more apparent here, with an entry level fixed broadband subscription costing 260% more than an entry level mobile broadband subscription.

Takeaways

- The demand for data is rising rapidly across the world. Bandwidth consumption increased by a third between 2015 and 2016, with the greatest increase in demand coming from the Africa region.

- The high cost of fixed broadband is inhibiting adoption. The price gap is so extreme in LDC regions, that mobile broadband remains the only feasible option there.

- Fixed broadband connection speed remains slow in developing countries. Excluding China, the penetration rate for high-speed connections (>10 Mbit/s) is a paltry 1.6%.

- Developing Countries and LDCs are now using fibre for fixed broadband connections, skipping over cable and DSL for the most part. As fibre penetration increases further, we can expect average speeds to rise as well.

{kind=link}