The global smartphone industry is going through a tough phase. The second quarter of 2023 marked the 8th consecutive quarter of a year-over-year (YoY) decline in smartphone shipments worldwide. According to the latest report from IDC, global smartphone shipments in Q2 2023 declined a staggering 7.8% YoY, resulting in just 265.3 million units shipped. On a quarterly basis, the industry witnessed a 1.22% decline in shipments.

The decline is even more surprising as it brought the worldwide shipments of smartphones to its lowest point since Q3 2013, when the shipment figure stood at 261.7 million. Even though major smartphone manufacturers pulled out all the stops, equipping their devices with mind-blowing features, cutting-edge specs, and the much-hyped 5G technology, the demand for their devices has hit an all-time low.

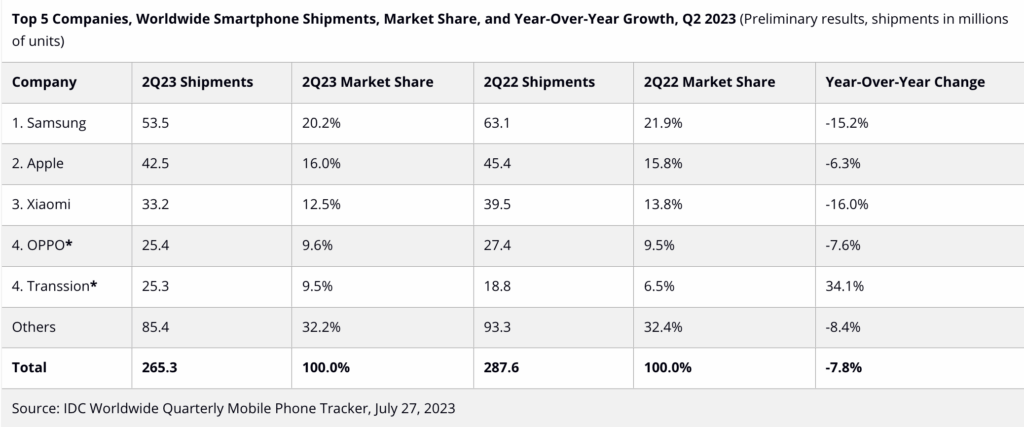

Additionally, among the top five smartphone brands globally, four of them reported a yearly decline in shipments, indicating that the slump is affecting even the biggest players in the market. This shipment decline is attributed to several factors, including soft demand, inflation, macroeconomic uncertainties, and excess inventory. However, there is a glimmer of hope as the rate of YoY decline in smartphone shipments appears to be slowing down when compared to the double-digit drops reported in the previous quarters. In Q4 2022 and Q1 2023, the worldwide smartphone industry recorded alarming declines of 18.31% YoY and 14.59% YoY, respectively.

Now, let’s delve into how the top five smartphone brands performed in terms of shipments and market share during Q2 2023.

Top 5 Smartphone Brands Q2 2023

- Samsung continues to be the market leader with a 20.2% shipment share during the second quarter of 2023, albeit down from 21.9% a year-ago period. The Korean giant recorded a notable 15.2% YoY decline in shipments during the second quarter, from 63.1 million units in Q2 2022 to 53.5 million units in Q2 2023.

- Among the top five smartphone companies in the world, Apple recorded the lowest decline of 6.3% YoY in iPhone shipments. This consistent trend of minimal decline has been observed over the past few years, showcasing the Cupertino giant’s ability to maintain a steady position amidst challenging times. Apple shipped 42.5 million iPhones in Q2 2023, accounting for 16.0% share of the global smartphone shipments.

- Xiaomi’s struggle continued in Q2 2023 as well, experiencing the highest decline of 16% YoY among the top five smartphone companies worldwide. The Chinese player shipped only 33.2 million units during the June quarter, accounting for a 12.5% market share. Several factors contributed to Xiaomi’s smartphone shipment decline during this period, particularly in its key markets of India and China, including innovative product launches, ED raids, the departure of Manu Jain, competition from other players, etc.

- Maintaining its 4th position, Oppo shipped 25.4 million units of smartphones worldwide in Q2 2023, however, with a 7.6% YoY decline. The Chinese OEMs is currently holding a 9.6% market share.

- A notable development in the smartphone market for Q2 2023 was the entry of Transsion into the top five list, surpassing Vivo. This Chinese manufacturer achieved an impressive 34.1% YoY growth in smartphone shipments, rising from 18.8 million units in Q2 2022 to 25.3 million units in Q2 2023.

- Notably, IDC has declared a statistical tie between Oppo and Transsion, as the difference in their share of revenues or shipments is minimal, at 0.1% or less. This showcases Transsion’s remarkable performance in the market, securing its place among the leading smartphone companies and challenging its competitors with significant growth.

In Q2 2023, China’s smartphone market witnessed a year-over-year decline of 2.1%, showing signs of improvement compared to the previous five quarters of significant double-digit contractions. Despite this progress, consumer sentiment and spending in China remain low, impacting the overall demand for smartphones in the region.

Even during the highly anticipated 618 online shopping festival in June, which was expected to boost sales, there was a 6.5% YoY drop in China’s smartphone sales.

Similarly, other major regions also encountered shipment declines in 2Q23: Asia/Pacific (excluding Japan and China) witnessed a decline of 5.9% YoY, the United States saw a significant 19.1% YoY drop, and Europe, the Middle East, and Africa (EMEA) experienced a 3.1% YoY decline in smartphone shipments.

What Industry Experts Have to Say

According to Nabila Popal, research director with IDC’s Mobility and Consumer Device Trackers, there is positive news for the smartphone market. Inventory levels are showing improvement, and there is optimism from key OEMs and supply chains as excess inventory in finished devices and components is expected to clear up by Q3 2023. This normalization of inventory levels is likely to lead to the market returning to growth by the end of the year and into 2024.

As the market ramps back up, there is an opportunity for vendors to gain share, and IDC anticipates a fascinating shift in the vendor rankings at the bottom of the stack. A notable example of this is Transsion entering the list of top 5 smartphone OEMs for the first time in Q2 2023. This indicates that the smartphone industry is witnessing dynamic changes and presents new opportunities for companies to assert their positions and achieve growth in the coming periods.

Anthony Scarsella, research director, Mobile Phones at IDC, believes opportunities are ahead in the second half of the year despite challenges in the first half.

The foldable smartphone market, in particular, continues to captivate consumers with its innovative appeal. With the introduction of new models and vendors, foldable technology is poised for wider adoption and lower prices, making it even more appealing to tech enthusiasts. IDC expects the global foldable market to grow by almost 50% YoY in 2023. This remarkable surge is anticipated to happen even though the overall smartphone market may continue to face some downturn.

Another report from Counterpoint Research reveals that global foldable smartphone shipments will exceed 100 million units by 2027, with Samsung and Apple leading the market.

Despite facing challenges in the first half, the smartphone industry seems to hold promising opportunities for growth and transformation in the coming periods. With new players entering the top ranks and the increasing demand for foldable devices, can the global smartphone industry anticipate a rebound in the second half of 2023? Let us know in the comment section!

{kind=link}