In 2023, Indian enterprises and startups encountered significant challenges in terms of investments and strategic business expansion, as revealed in PWC India’s latest report titled “Deals at a Glance.” The report paints a stark picture of a substantial decline in both deal volume and value for private equity (PE) and mergers and acquisitions (M&A) deals throughout the year. Notably, startups experienced a challenging period, marking the lowest fundraising figures in the past five years.

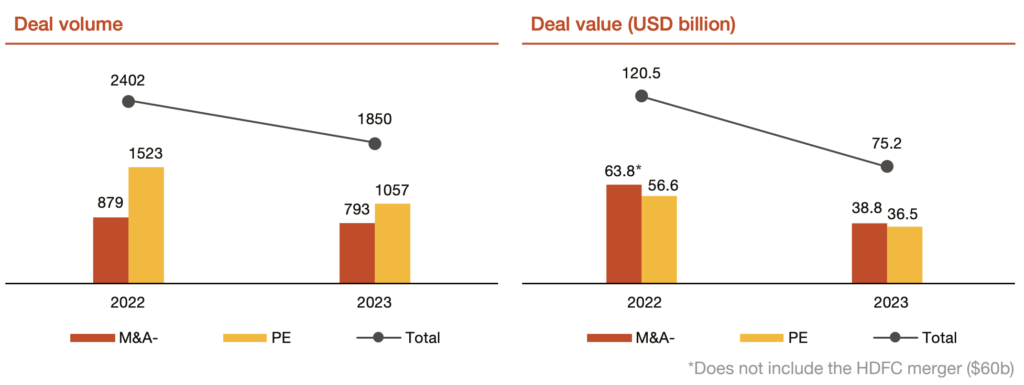

The combined value of deals, encompassing both PE and M&A, declined a significant 23% YoY in CY 2023 to 1850. Simultaneously, the total value of these deals plummeted a massive 37.6% YoY to $75.2 billion during last year.

In particular, M&A deals totalled 793 in volume in 2023, with a drop of 9.8% YoY. However, the more striking aspect lies in the substantial decline in the total value of these M&A deals, which plummeted by a massive 39.3% YoY, amounting to $38.8 billion for the year.

The state of Private Equity (PE) investments in Indian companies in 2023 is even more concerning, with a notable decline of 30.6% YoY in deal volume and a strong 35.6% YoY drop in value. This translated to 1,057 PE deals with a cumulative value of $36.5 billion during the same period.

Despite the overall contraction in the investment landscape, a notable shift occurred between 2022 and 2023 – the average investment size per deal increased from $42 million to $46 million. This suggests a potential strategic shift towards pursuing larger and more impactful opportunities within the Indian market.

Early-Stage Woes, But Buyouts Show Resilience

The early-stage investments in Indian companies witnessed a significant 53% YoY decline in CY23. However, despite this reduction, both early-stage and growth-stage investments combined continued to dominate, accounting for a significant 73% of the total funding during the year.

Surprisingly, buyouts demonstrated resilience with only a 5% decline in CY23 compared to CY22, indicating a heightened level of investor activity in acquiring well-established companies. This trend implies a strategic shift towards more mature and proven ventures, reflecting investor confidence in such entities.

Top Sectors

- India’s retail and consumer sector took the lead as the champion in both deal volume and value, boasting 289 deals with a total value of $8.8 million in 2023.

- The technology sector secured the second position with 269 deals in volume and a total value of $4.6 million last year.

- Notably, the financial services, renewable power, and healthcare sectors, although ranking 7th, 8th, and 5th in terms of deal volume, emerged as the 2nd, 3rd, and 4th in terms of deal value, respectively.

- In 2023, companies in India’s fintech sector clinched 130 deals with a combined value of $2.9 million, underscoring the sector’s robust performance and significant investment activity.

Indian Startup Funding: A 5-Year Low

In 2023, the Indian startup ecosystem grappled with a significant funding downturn attributed to global economic uncertainties and the looming threat of recession. These challenges triggered extensive restructuring efforts and widespread layoffs within the industry. Surprisingly, the funding raised by Indian startups declined 68% YoY to just $8 billion in 2023, the lowest in the last 5 years. The average ticket size for these fundings was $13 million.

The top five sectors attracting substantial investments were SaaS, D2C, LogiTech and AutoTech, FinTech, and e-commerce B2B.

Despite the overall funding challenges faced by Indian startups in 2023, what adds an intriguing dimension is the dominance of growth and late-stage deals. Together, these categories accounted for approximately 85% of the total funding secured last year. Interestingly, the average ticket sizes were around $21 million for growth-stage and $47 million for late-stage deals. This suggests a clear investor inclination towards supporting more established and mature startups, signalling a strategic move away from early-stage ventures. This strategic move could be attributed to a cautious approach aimed at mitigating risks and ensuring a focus on ventures with proven track records and potential for significant impact.

{kind=link}