In the dynamic world of Indian finance, the first half of the fiscal year 2023-24 (H1 FY’24) has brought forth intriguing trends in initial public offerings (IPOs) and public equity fundraising. According to the PRIME Database, Indian companies took centre stage in a tale of two periods: one marked by a significant yearly decline in main board initial public offerings (IPOs) and the other by a surge in fundraising efforts when a particular mega-IPO is excluded.

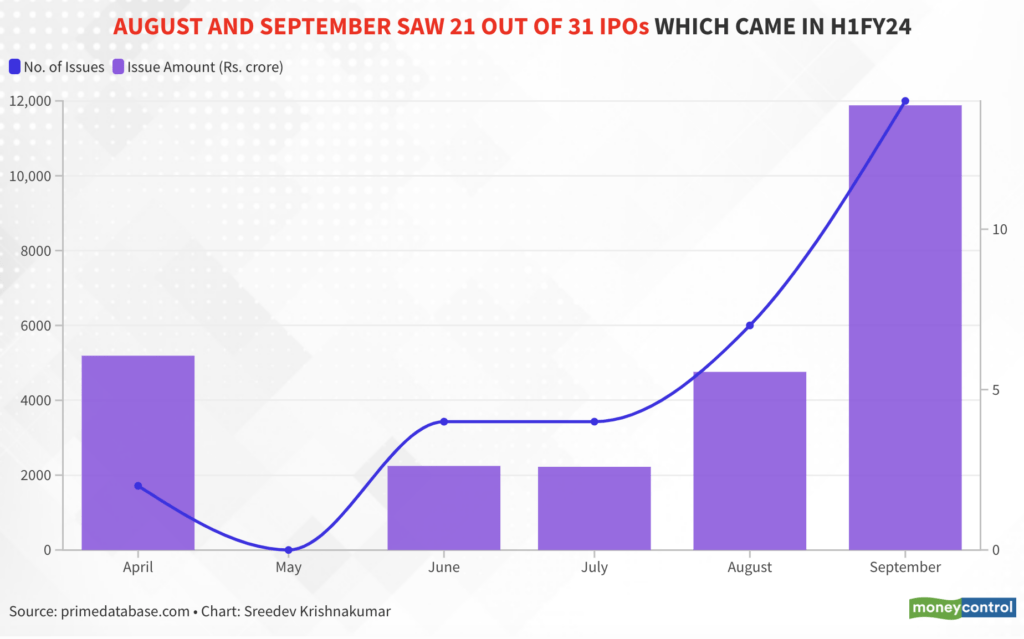

The amount of funds raised by Indian companies through IPOs declined 25.8% YoY in the first half of fiscal year 2024 (from April to September). A total of 31 companies went public, collectively raising Rs 26,300 crore in H1 FY24 compared to the Rs 35,456 crore raised by 14 companies via IPOs in H1 FY23.

What’s especially eye-catching is the timing of these corporate companies going public. Remarkably, out of the 31 IPOs that graced the public market in H1 FY24, 21 debuted in August and September, creating a buzz of excitement in the financial world.

The largest IPO during H1 fiscal 2024 was from Mankind Pharma, raising a whopping Rs 4,326 crore. This IPO occurred from April 25, 2023, to April 27, 2023. Following suit, JSW Infrastructure made a strong showing, securing Rs 2,800 crore in its IPO conducted between September 25, 2023, and September 27, 2023. In contrast, Plaza Wires opted for a more measured approach, conducting a commendable IPO from September 29, 2023, to October 4, 2023, which successfully secured Rs 67 crore.

What’s truly attention-grabbing is the stark contrast in the size of the largest IPOs between H1 FY24 and H1 FY23. Notably, the largest IPO in H1 FY23 is nearly 5x the size of its counterpart in H1 FY24. The elephant in the room was the massive LIC IPO, conducted from May 4 to May 9, 2022, which raised an impressive Rs 20,500 crore. However, when we exclude this colossal outlier from the equation, we witness a striking 76% surge in IPO mobilization during the current fiscal year. This indicates a significant uptick in the overall activity and enthusiasm surrounding IPOs.

In the grand fundraising scheme through IPOs, including SME IPOs, the collective numbers for H1 FY23 and H1 FY24 were Rs 36,594 crore and Rs 29,032 crore, respectively. The pinnacle of this IPO bonanza was reached in H1 FY22 when the figures soared to an astonishing Rs 52,325 crore. This marked an astounding 578.4% YoY surge from the relatively modest Rs 7,713 crore raised in H1 FY21.

During the first half of fiscal 2022, market giants like Zomato and CarTrade made their significant IPO debuts, contributing to the record-breaking figures.

“Notwithstanding the present volatility in the secondary market, the next four to five months are likely to see several IPOs being launched before a pause on account of the general elections,” said Pranav Haldea, Managing Director, PRIME Database Group.

BFSI and New-Age Tech Firms Take a Backseat

The first half of fiscal year 2023-24 has revealed some intriguing shifts in the IPO landscape, particularly in terms of sector participation.

In H1 FY24, fundraising through IPOs saw a notable drop, particularly in the banking, financial services, and insurance (BFSI) sector, which contributed just Rs 1,525 crore or a mere 6% of the total funds raised. This is a significant departure from H1 FY23, when the BFSI sector dominated the IPO scene, accounting for a substantial 61% of IPO funds.

Furthermore, there was a lack of participation from new-age technology companies (NATC), with only one out of the 31 companies going public falling into this category. This can be attributed to several factors, including economic slowdown, fundraising challenges, concerns about an impending recession, and significant layoffs within the tech sector, all collectively contributing to a notable slowdown in IPO activity.

Nevertheless, the future holds promise and potential for a resurgence in tech IPOs. New-age tech companies have been diligently working towards profitability, making strategic decisions to optimize costs while maintaining robust growth. This concerted effort is expected to yield a substantial pipeline of IPO-ready companies in the next five years.

A fascinating trend has emerged in India’s stock market, particularly in the participation of the general public and retail investors.

Overwhelming Public Response: The explosion of smartphones and the emergence of platforms like Zerodha and Groww are democratizing IPO participation in India, making it more accessible and appealing to the general public.

Despite the overall decline in fundraising, there was a significant level of public participation in IPOs. Of the 28 IPOs for which data is available, 19 were more than 10 times oversubscribed. Nine of these IPOs even attracted more than 50 times oversubscription. Additionally, four IPOs were oversubscribed by more than three times, while five others were oversubscribed between one and three times.

The high net worth individual (HNI) segment, consisting of individuals with investments ranging from Rs 2 lakh to Rs 10 lakh, showed strong interest, with 17 IPOs receiving more than 10 times oversubscription.

Retail Investor Enthusiasm: Retail investors didn’t want to miss out on the action either; they have demonstrated heightened interest in IPOs, with the average number of applications increasing to 10.02 lakh, compared to 7.57 lakh in FY23. Notably, the Ideaforge IPO received the highest number of applications from retail investors at 22.29 lakh, followed by Aeroflex at 21.62 lakh, and SBFC Finance at 20.19 lakh.

The Appeal of Listing Gains: Another factor contributing to the IPO market’s appeal was the average listing gains, which reached 29.44% in H1 FY24, a substantial increase from the 11.56% recorded in H1 FY23. These strong listing gains further fueled investor interest in IPOs.

As the Indian IPO landscape continues to evolve, it’s evident that several factors, including sector preferences, public participation, and market dynamics, are shaping the trends. While the first half of the fiscal year has shown both peaks and valleys, it remains to be seen how the Indian IPO market will unfold in the second half of the current fiscal year (Oct 2023 – March 2024), especially with the backdrop of general elections that are on the horizon.

{kind=link}