Old habits die hard. An adage, it stands true for Indians and their long-standing preference for cash. As per recent reports, Indians have, most likely, retrogressed to their old habit of cash payment. An analysis of credit and debit card usage for the previous fiscal year indicates that this situation arose in wake of the improvement in currency circulation. Currency with the public has chartered ceilings of over Rs 18.5 lakh crore as on May 25, 2018. This is considerably more than double from Rs 7.8 lakh crore in December 2017, the post-demonetization decision in late 2016, as per RBI data.

When Narendra Modi led government withdrew 86% of the country’s currency, one of the many motives was to boost digital transactions in India and reduce the use of cash. Debit card payments outstripped the past credit card usage immediately after demonetization and the government’s digitization agenda got the required thrust.

However, this economic-shift was fugitive and plainly, didn’t last long. Credit card transactions inched past debit card payments in August 2017 as cash began retreating into it’s coveted space and has entrenched its roots, since.

As per the latest data released by the Reserve Bank of India, the value of credit card transactions peaked to a 15-month high of Rs 44,308 crore in March 2018, as compared to Rs 41,857 crore for debit card payments.

Indian’s Unwavering Love For Cash

Cash withdrawal by individuals during January-March 2018 was at Rs 1.4 trillion, which was apparently a considerable rise from Rs 1.1 trillion in the corresponding quarter of 2016.

As an instance, the upper class cannot always use credit cards or make cashless payment for routine activities like purchasing vegetables, groceries, medicines, etc. because hard-up, average vendors don’t have a bank account or use apps like PayTM or BHIM.

As per reports, almost all non-cash payments transactions have declined. In April 2017, the transaction value of UPI rose to Rs 2,450 crore from Rs 2,200 crore, standing alone as an exception to the above-mentioned decline. However, the number of transactions aren’t accountable as of now, since it has been just a year-old addition to the digital payments.

However, as the pace at which currency in circulation has been growing, all other electronic payment channels have witnessed a fall-off in the transaction. Citing a relevant instance, the value of National Electronic Funds Transfer (NEFT) transactions fell from Rs.12.15 trillion to Rs.10.40 trillion, down 14.4% for the previous year.

Why Are Indian ATM’s Running Dry?

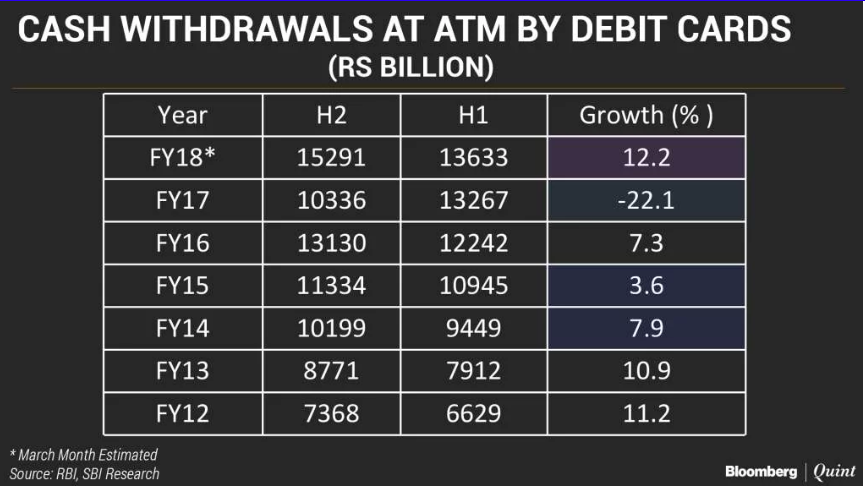

Cash withdrawals at ATM is another gauging specimen to track the change in Indian cash habits, post demonetization. It also gives an inkling to the recent cash crunch.

Data on the monthly transactions at ATM suggests that the cash demand at ATM, soared up as soon as cash availability improved in the months, post demonetization.

The latest crisis of cash machines, running dry, proves that both India’s central bank and the government have severely undervalued Indian consumer’s unwavering preference for cash. The short-lived rise in the volume of electronic payments may be one reason for the blunder, wherein even the RBI missed signals and dropped the ball.

The RBI whipped into shape by blaming it on logistic issues in the cash machines. In the press release, they added that these ATMs are still being replenished to dispense newer denominations to account for specific sizes. Still and all, there’s been an assurance from RBI to print more notes to meet the increased demand for cash.

A Rough-And-Ready Banking System

The government’s hope of witnessing a better socio-economic spectrum, where people are less reliant on cash, seems more of a head-trip since irrespective of rigid measures, the implementation is not-profitable. Digitization, being one such obligatory course during the demonetization drive, although not completely a sinking-ship, has only managed to encompass a specific periphery with the electronic payments. Despite the hype over electronic payments, consumer preference for cash remains unaltered.

{kind=link}