The US mobile data market now contributes to 46% of the revenue in US mobile industry. It has grown 4% QoQ and 14% YoY and is now a 21$ Billion industry, which is expected to reach 90$ Billion by end of 2013. Technically, mobile data is pegged to Smartphone and the adoption of mobile internet, network upgrades and new smartphone connections derive the growth of mobile data.

Smartphone industry in the US is largely penetrated by Apple iPhone, followed by Android-powered Samsung devices. In 2012, the situation was upside down and Samsung dominated the US Smartphone market. However, if we pay close attention on trends of first half of the year, Apple has leapfrogged Samsung. And, the trend is going to continue if ever Apple decides to introduce its low-price iPhone, purported as iPhone 5C scheduled for Sep 10 launch, in US market.

The number of new connections in the second quarter have been lowest in history and decreased by 95% over quarter to 139K. U.S. market has 240M subscribers maintaining 335 million subscriptions. Out of 240 million Subscribers, 145M are supposedly using smart phones. Besides, if we fish out the number of subscribers who falls under the age group (0 -5 years), many newborn gets iPhone as welcome gift, the left over number of subscriptions remain 293 million. So it’s a clear fact that more than 50% of mobile subscriptions are active on non-smartphone devices, indicating that market is healthy and speculations complaining about the growth of smart phone sales can brushed aside.

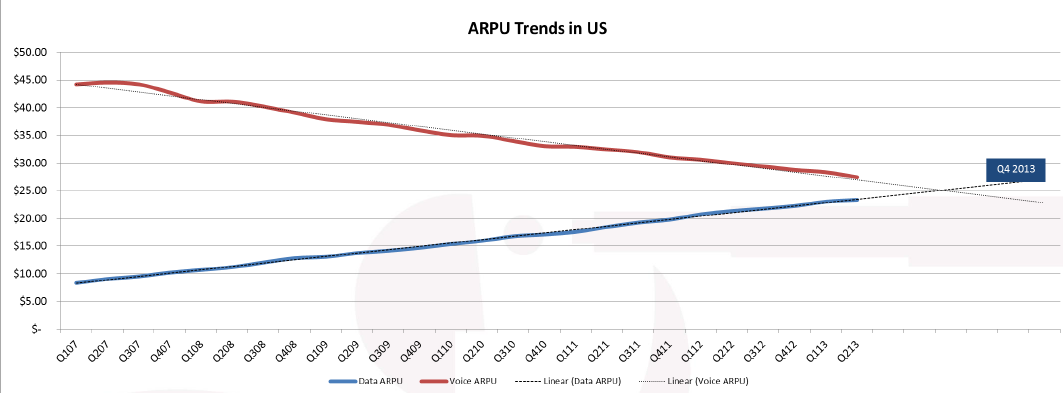

The ARPU (Average Revenue Per User) is decreasing due to latest technology and tough competition, predominantly most of the ARPU was from calls but now ARPU from data is fast growing. We can see the trend and comparison between ARPU from Calls and Data

We can see how gradually the Call usage is decreasing drastically, Usage of internet, VoIP, Social Networking, Faster Data Speeds all have significantly contributed to this change. The overall ARPU has declined by 0.57$, call ARPU by 1.17$ and data ARPU grew by 0.61$ this quarter. And according to the graph the Data ARPU is expected to dominate Call ARPU by the end of this year.

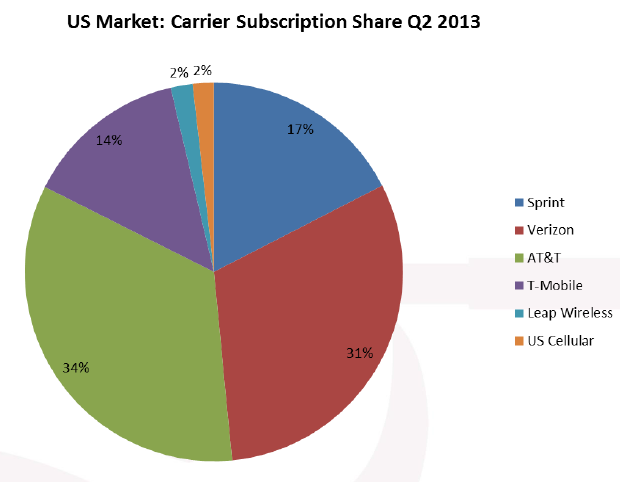

Verizon and AT&T still continue to be the market leaders accounting to 71% of the revenues generated by mobile data services and 65% of the subscription base. This quarter has been really good for T-Mobile ,experiencing positive growth for the first time after 12 quarters and more over for the first time in 6 years T- Mobile has come out to be the leader in Net-adds beating Verizon by a small margin. AT&T continues to lead the connected device segment with 48% of the market share.

AT&T and Verizon have launched shared data plans which gave positive results. This service enables the user to subscribe to a particular data plan from mobile phone and use that data simultaneously by laptop , tablet , home Hotspot , Wireless Home phone . Families with multiple devices are greatly benefited by this service and many American families are opting out for this choice.

The report calls for a need of Fourth wave services to capture the next Trillion dollars from the smart phone Industry. A structure frame work is required to generate more revenues. And integration of mobiles and data to more activities like digital life and home security solutions and similar such integrations can bring new dimensions to the industry. The mobile Market in US is still thirsty and can absorb more than speculated, coming to global market the scenario is still fertile and enormous amounts of growth potential exists.

Source: Mobile Future Forward.