Now, disputes related to refresh 2G spectrum auction in India has got over. The government has failed to generate expected INR 400 billion from the refresh auction; they could generate just INR 94.1 billion (US$1.71 billion) from the auction.

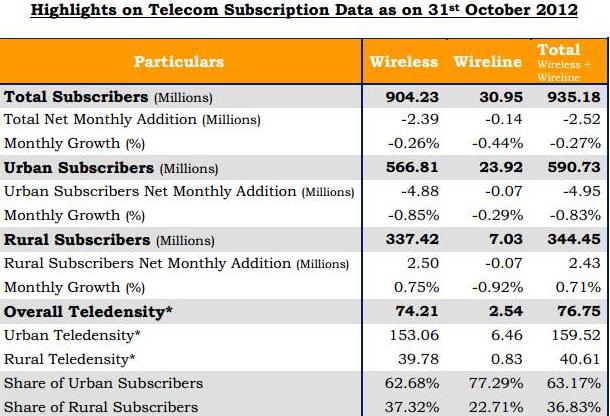

In India, telephone subscribers base (wireless + wireline) decreased to 935.18 million at the end of October this year, from 937.70 million in September. In other words, overall telecom subscriber base plunged 0.27% month-over-month in October. On the other side, overall teledensity of the country also reached to 76.75 at the end of October this year, from 77.04 of the previous month.

Urban telecom subscriptions decreased to 590.73 million at the end of October 2012, from 595.69 million in September this year. Although urban areas showed off modest month-over-month decline (0.83%) in October, but rural subscription base somehow succeeded to offset the overall decline.

Wireless Subscriber Base:

In October, total wireless subscriber base decreased to 904.23 million, representing 0.26% monthly decline, from 906.62 million in September this year. The decline in the last month was due to many disconnections (subscriber base, based on some terms and conditions) by some of the service providers. The proportion of wireless subscribers in urban areas dropped in the last month, whereas rural India showed significant growth during the same period, from 36.94% to 37.32%.

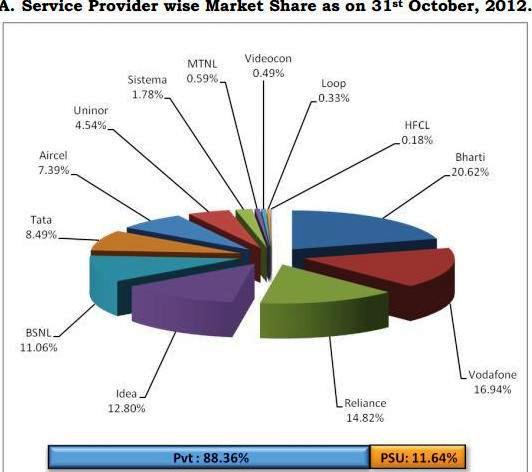

As usual, private operators succeeded to hold dominance with 88.36% of the wireless market share (based on subscriber base) in October. In the context, PSUs (BSNL and MTNL) managed to hold only 11.64% market share. Most important point here is that, active wireless subscriber reached to a peak level in the month of October 2012. Apparently, it could be one of the great hearsay for telecom operators. There were 703.92 million active VLR (visitor location register) for the month of October, approximately 77.85% of the total wireless subscriber base.

In circle-wise, J&K had highest proportion of VLR subscribers with 85.16% in October, followed by Maharashtra and Assam with 83.62% and 82.34% respectively. In contrast, Tamil Nadu reported lowest proportion (69.18%) of VLR in October this year. In terms of VLR, Idea led with 95.37% figure in October, followed by Bharti Airtel with 91.72%.

Mobile Portability:

In October 2012, 75.14 million subscribers submitted their requests to different service providers for porting mobile number. In Northern & Western India (MNP Zone-1), Rajasthan reported highest requests (7.15 million) for number portability, followed by Maharashtra (6.51 million). On the other side, in Southern & Eastern (MNP Zone-II), Karnataka received highest number of requests (9.37 million) and Andhra Pradesh with 7.02 million requests in October 2012. In September this year, 5.36 million subscribers submitted their requests for MNP.

In October, wireline subscriber base also plunged to 30.95 million, from 31.08 million at the end of September 2012. Net reduction in wireline subscriber base was reported 0.14 million in October. More importantly, wireline subscriber base in urban sector augmented from 77.17% to 77.29%, whereas rural subscriber base declined from 22.83% to 22.71%.

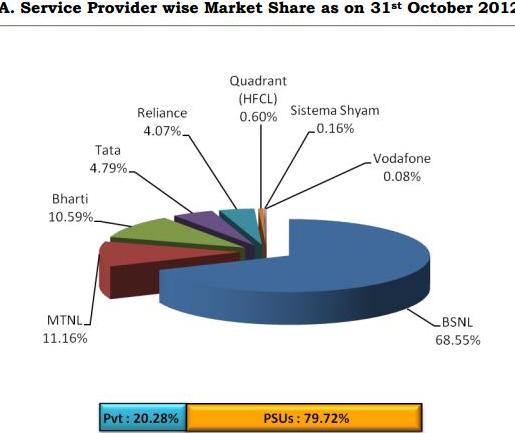

Unlike wireless market share, PSU reported 79.93% of their hold in the market in terms of wireline subscriber base in October this year.

Broadband Subscriber Base In India:

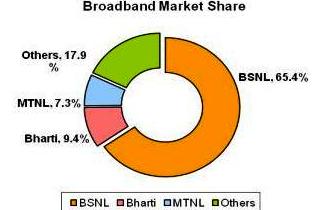

Broadband subscriber base in India soared up from 14.68 million at the end of September 2012 to 14.81 million as of October end, representing 14.10% and 0.89% Y/Y and M/M (month-over-month) growth respectively. Until the end of October 2012, India had 157 Internet Service providers (ISPs). Furthermore, only 113 ISPs provided data for the month of October 2012 to subscribers in India. See the image (below) for broadband market share of vibrant ISPs:

In October, BSNL had highest (9.69 million) broadband subscriber base, followed by Bharti Airtel and MTNL with 1.39 million and 1.08 million subscribers respectively.

However, it’s true that overall telecom subscriber base in the country has gradually been declining over past few months. But as active wireless subscriber base has uniformly increasing month-over-month, it could be lucrative for telecom vendors to generate more revenue. The reason is quite obvious that average revenue per user (ARPU) depends upon active users, but not total subscriber base. The main problem in India is that a significant number of subscribers are having multiple SIMs, and most of them (SIMs) remain unused.

Source: TRAI